This is the notes of Continuous Stochastic Structure Models with Apllication by Prof. Vijay S. Mookerjee. In this note, we are talking about Stochastic Process, Parameter Estimation, PDE and Stochastic Control.

Stochastic process

- Brownian Motion (BM): $Z_t \sim \mathcal{N}(0,t)$;

- Arithmetic Brownian Motion (ABM): $d \mu = \alpha dt + \sigma dZ_t$

- Geometric Brownian Motion (GBM): $dY_t = (\alpha + \frac{1}{2} \sigma^2) dt + \sigma dZ_t$

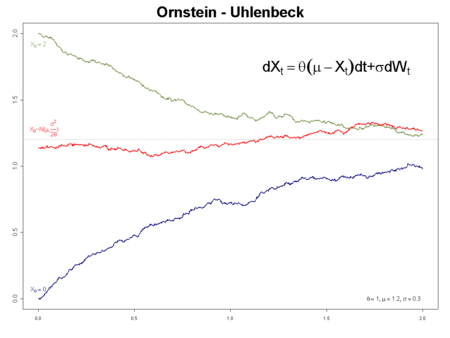

- Ornstein-Uhlenbeck process (O-U Process): $du = \alpha(\mu-u)dt + \sigma dZ_t$, where $\alpha$ is speed of reversion and $\mu$ is long-term mean (A.K.A steady state mean). The distribution of O-U Process is $u \sim \mathcal{N} (\mu_{\mathcal{N}}, \sigma_{\mathcal{N}})$, whereAs $t \rightarrow \infty$:

- if $\alpha > 0$,Converge.

- if $\alpha = 0$,Diverge.

- if $\alpha < 0$, Diverge.

- Cox-Ingersoll-Ross (CIR) process: $dX_t = \alpha (\mu-X_t)dt+\sigma \sqrt{X_t} dZ_t$

- Stochastic Differential Equation for general 1-Spatial dimension Itô drift-diffusion process: $dX_t = \mu(X_t,t)dt + \sigma(X_t,t)dZ_t$

- Ito’s lemma: $Y$ is Itô drift-diffusion process, $f: \mathbb{R}^2 \to \mathbb{R}$ is smooth, then$(dt)^2 = dt dW_t$; $(dW_t)^2 = dt$

Parameter Estimation

- Using Maximum Likelihood Estimation (MLE):

- Exact MLE: Using known density function $f(x_i|\theta)$;

- Inexact MLE:

- First Difference Maximum Likelihood Estimation (FDMLE)1

- Fokker Planck Equation

- Fokker Planck Equation:

Partial Differential Equation

- General linear second order Partial Differential Equation (PDE)23:

- Elliptic: if $B^2-AC < 0$. Simple example is 2-D Laplace Equation: $u_{xx} + u_{yy}= 0$ (where $X = x$, $Y = y$, $A = 1$, $B = 0$, $C = 1$), which can describe the electrostatic field.

- Parabolic: if $B^2-AC = 0$. Simple example is 1-D Heat Equation: $u_t - K u_{xx} = 0$ (where $X = x$, $Y = t$, $A = -K$, $B=C=0$), which can describe heat transportation process

- Hyperbolic: if $B^2-AC > 0$. Simple example is 1-D Wave Equation: $a^2 u_{xx} - u_{tt} = 0$ (where $X = x$, $Y = t$, $A = a^2$, $B = 0$, $C = -1$), which can describe light wave.

- MATLAB function

pdepecan solve initial-boundary value problems for parabolic-elliptic PDEs in 1-D.

Stochastic Optimal Control Process

Stochastic Control problem concept:

- Agent

- State: $X_t$, SDE:

- Control: $u(X_t,t)$

- Objective Function: $F(u, t)$

Using Brand Management on Twitter as an example:

- Agent: Some firm, such as AT&T Co.

- State: Sentiment Score of customers on Twitter;

- Control: Effort AT&T Co. pay to increase the sentiment;

- Objective Function: Return;

If we want to minimize value function:

where $\gamma$ is discount factor.

Taylor expansion on $\eqref{1}$:

- $\eqref{2}$ into $\eqref{1}$:

- Hamilton-Jacobi-Bellman (HJB) equation is a partial differential equation which is central to optimal control theory. The solution of the HJB equation is the value function which gives the minimum cost for a given dynamical system with an associated cost function.

Expectation on $\eqref{3}$: - Guess Objective Function (such as the return of the firm) follow the form of $F(u, t) = \beta X - C u^2$. Drift term of State $dX_t$ follow the form: $f(u, t) = k_1 u \sqrt{b-X} - k_2 X$; Volatility term of State $dX_t$ follow the form: $g(u, t) = k_3$. Thus replace $f$ and $g$ in $\eqref{4}$ HJB equation:

- Optimal Control: Partial derivative of the term inside $Max_{u(X, t)}$ in RHS w.r.t. $u$:

- Guesswhere $\lambda_1 > 0$, $V_X = \lambda_1$, $V_{XX} = V_t = 0$. Substitute $\eqref{5}$ and $\eqref{6}$ into $\eqref{4*}$:

- (X) part of $\eqref{7}$:

- (Constant) part of $\eqref{7}$:

- Solve $\eqref{8-1}$ and $\eqref{8-2}$ ($\lambda_1 > 0$):

- Substitute $\eqref{9-1}$ and $\eqref{9-2}$ in $\eqref{5}$:

- Substitute $\eqref{10}$ in $\eqref{0}$, note that $f(u, t) = k_1 u \sqrt{b-X} - k_2 X$, $g(u, t) = k_3$:Define:Then $dX = \alpha_{HJB} (\mu_{HJB} - X) dt + \sigma_{HJB} dZ$, which is O-U process!

- According to O-U Process, state $X \sim \mathcal{N} (\mu_{\mathcal{N}}, \sigma_{\mathcal{N}})$, where converge with $t \to \infty$ when $\eqref{12-1}$ $\alpha_{HJB} > 0$.

Read More

- UTDallas-OPRE7320: Optimal Control Theory: Chap 13 Stochastic Optimal Control:

- Princeton-Economics 521, Advanced Macroeconomics I:

Lecture 4: Hamilton-Jacobi-Bellman Equations, Stochastic Differential Equations

Lecture 5: Stochastic HJB Equations, Kolmogorov Forward Equations

1. Han, C., & Phillips, P. C. (2013). First difference maximum likelihood and dynamic panel estimation. Journal of Econometrics, 175(1), 35-45. ↩

2. Partial Differential Equations in Finance ↩

3. Stanford MATH220a: 4 Classification of Second-Order Equations ↩